By Meenakshi Chauhan

Associate Director – ESG, Process and Performance Enhancement

MGC Global Risk Advisory

ESG is at an inflection point. What was once treated as a disclosure obligation has become a defining test of corporate credibility. In 2026, sustainability claims are assessed with the same skepticism and rigor applied to financial performance.

Regulators, investors and boards are aligned around a single expectation: ESG assertions must be grounded in auditable, decision-grade data.

This shift represents a fundamental change in corporate governance. ESG has moved beyond compliance checklists and reputational positioning into the core of enterprise accountability. Sustainability is being

re-engineered from narrative to evidence, from intent to execution and from voluntary transparency to institutional responsibility.

Closing the Substantiation Gap

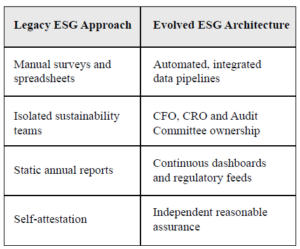

For more than a decade, ESG operated in a substantiation gap. Organizations made claims such as “carbon neutrality”, “ethical sourcing” or “net-zero alignment” without data architectures capable of supporting regulatory scrutiny or external assurance. While often well intentioned, these commitments lacked verification depth and increasingly exposed companies to legal, financial and reputational risk.

That gap is now being systematically closed. Regulatory frameworks including the EU Corporate Sustainability Reporting Directive (CSRD), the Green Claims Directive and India’s Business Responsibility and Sustainability Reporting (BRSR) mandate structured disclosures of ESG risks, controls and outcomes. Sustainability statements are treated as regulated representations with implications comparable to financial reporting.

As a result, ESG disclosures are increasingly governed with board oversight, internal controls and external assurance. The shift is clear:

- From promotional claims to provable outcomes

- From narrative disclosures to traceable evidence

- From symbolic assurance to audit-level scrutiny

ESG as a Financial and Risk Control System

Publishing sustainability reports is insufficient in a

high-accountability environment. Leading organizations are building ESG truth systems: enterprise-wide data infrastructures where sustainability metrics flow through ERP platforms, risk frameworks, internal controls and audit processes.

ESG governance is converging with financial governance. Sustainability performance is increasingly evaluated alongside capital allocation, enterprise risk and strategic resilience.

How Credibility is Being Built in Practice

Across markets and sectors, organizations leading the ESG transition are operationalizing credibility rather than amplifying ambition.

- Linking executive remuneration to sustainability outcomes and disclosing progress transparently, including underperformance

- Embedding supplier emissions, labor audits and responsible sourcing into procurement and risk systems with third-party validation

- Indian listed entities strengthening BRSR disclosures through structured data and assurance

- European companies integrating CSRD-aligned sustainability metrics into statutory filings and audit scopes

Capital markets are responding to demonstrated transition capability rather than aspirational targets. Measurable emissions reduction verified labor compliance and accountable governance increasingly influence valuation and access to capital.

Scope 3 and the Demand for Radical Transparency

The most complex credibility challenge sits within Scope 3 impacts, embedded across value chains. Traditional reliance on supplier questionnaires, industry averages and sampling-based audits does not meet contemporary accountability expectations.

Leading organizations are replacing these approaches with:

- Digital product passports linking materials to verified environmental and social attributes

- Supplier-level emissions accounting embedded within procurement systems

- Satellite and geospatial monitoring for land use, deforestation and extractive risk

- AI-driven labor analytics identifying forced labor, wage violations and safety risks

Scope 3 accountability is transforming sustainability into a supply-chain and operating-model discipline rather than a reporting exercise.

Assurance as the New ESG Currency

Independent assurance has emerged as the defining signal of ESG credibility. Sustainability information is increasingly evaluated through the same trust mechanisms that underpin financial markets.

Frameworks including BRSR, CSRD, International Sustainability Standards Board (ISSB), and Global Reporting Initiative (GRI) are accelerating the shift toward assured disclosures covering emissions, workforce metrics, safety, water and supply-chain practices. This evolution is driving:

- Reduced exposure to greenwashing and misstatement risk

- Higher data quality and stronger internal controls

- Increased investor confidence in ESG-adjusted decision making

The Authenticity Premium

In a fact-checked environment, flawless performance narratives undermine trust. The organizations that command credibility are those that disclose performance gaps with clarity and accountability.

They communicate:

- Where targets were missed

- Why outcomes diverged from expectations

- What corrective actions are underway and how progress will be measured

This transparency creates an authenticity premium. Stakeholders place greater confidence in organizations that demonstrate learning, adaptation and governance maturity rather than perfection.

Conclusion: ESG has Become a Credibility Mandate

The next chapter of ESG will be defined by systems, controls and verified outcomes rather than messaging. Sustainability performance is being embedded into financial governance, enterprise risk management and board oversight as a core measure of organizational resilience.

Organizations that succeed will distinguish themselves through evidence, not aspiration. Traceable data, assured metrics, transparent disclosures and accountable governance will determine trust, valuation and long-term legitimacy.

In a high-accountability economy, credibility is not claimed. It is proven.

For further information on strengthening ESG credibility, assurance and governance, please write to us at: talk-to-esg@mgcglobal.co.in

Read more on latest Leadership Opinions at Green Growth for MSMEs: How CSIR Is Driving Sustainable Manufacturing in India